SMM January 15, 2026 News:

The negotiations for 2026 secondary lead long-term contracts have largely concluded, yet the market presents an unprecedented complex landscape—the initiation of secondary lead long-term contract negotiations was delayed by 1-2 months YoY, the long-term contract proportion for most enterprises continued to narrow, the discount magnitude hit a four-year low, and some smelters even opted to exit the long-term contract system. Behind this shift lies both a reflection of profound adjustments in the pricing mechanism of the secondary lead industry chain and an indication of a fundamental transformation in the industry's operational logic.

I. Price Trend: Cost Transmission Behind Narrowing Discounts

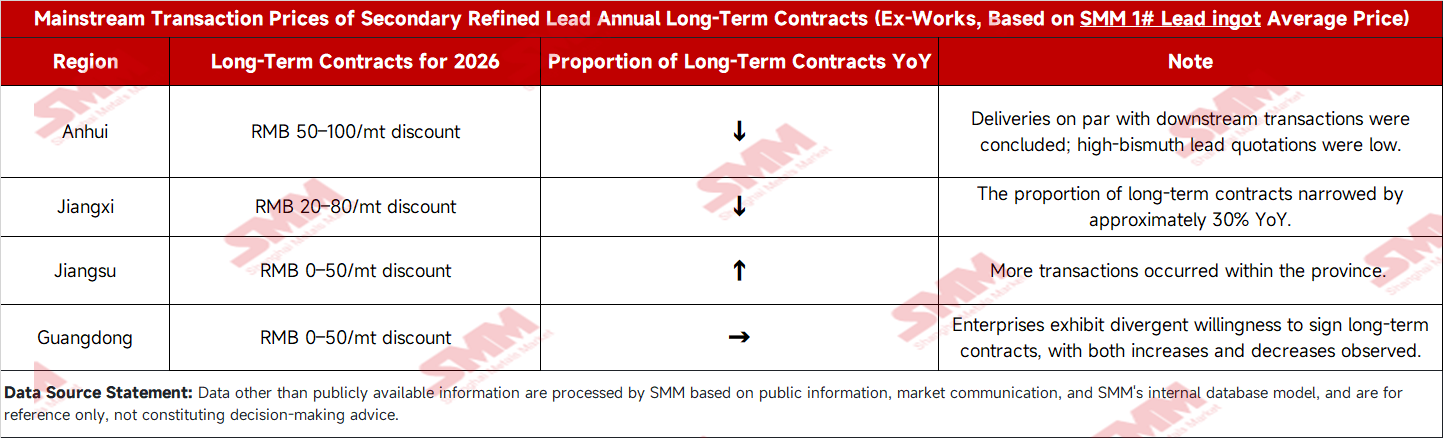

Data Comparison: The mainstream long-term contract prices for 2026 were at a discount of 80-20 yuan/mt against the SMM #1 lead ingot average price, narrowing by 50-0 yuan/mt compared to 2025.

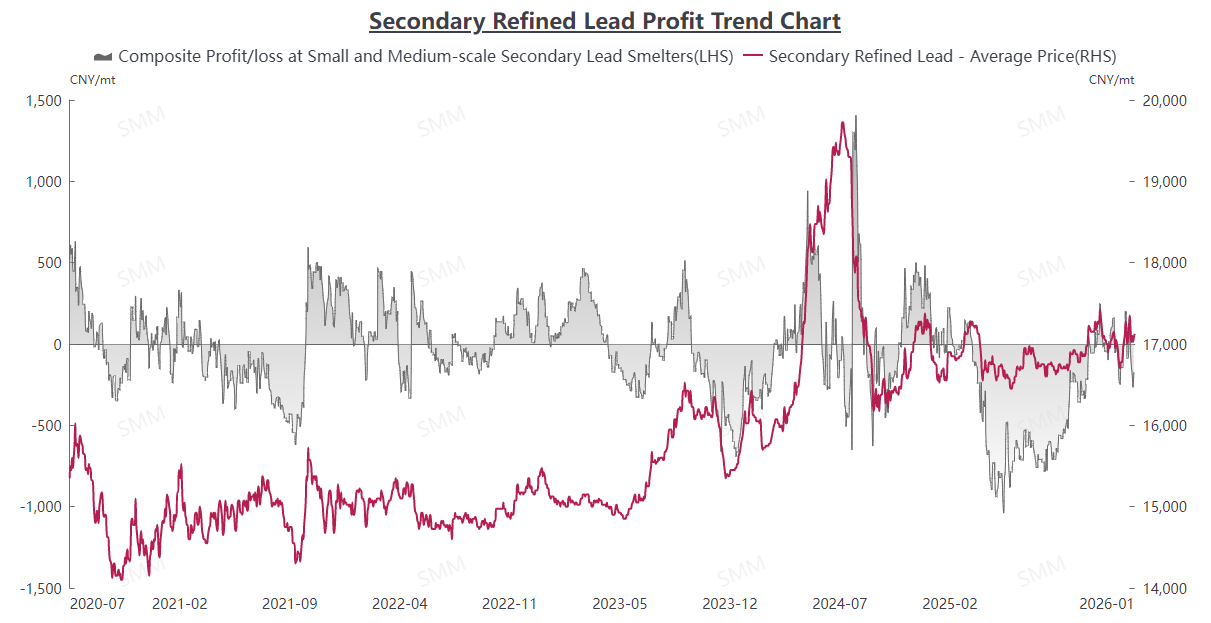

Cost Analysis: Scrap battery procurement costs rose 1.35% YoY, squeezing smelting margins.

Regional Differences: Pricing strategies diverged significantly in key production areas such as Anhui and Jiangsu.

II. Structural Changes: Restructuring of Long-Term and Spot Order Ratios

Ratio Changes: The long-term contract ratio generally narrowed, with the traditional 7:3 long-term to spot ratio often shifting to 2:8.

Enterprise Strategies: Some large enterprises maintained a high long-term contract ratio to secure capacity, while most large and small-to-medium enterprises preferred more flexible adjustments.

Downstream Choices: Some battery producers leaned towards extending the long-term contract settlement cycle, transitioning from monthly to quarterly settlements.

III. Market Divergence: Significant Split in Enterprise Willingness to Sign Contracts

Stance of the Adherents: Capacity-scale enterprises still require long-term contracts to ensure stable production.

Considerations of the Wait-and-See Camp: The need for operational flexibility and avoidance of price risk lock-in.

Factors for the Exit Camp: Uncertainty in industrial transformation regarding 2026 production, with output solely for their own groups.

IV. Underlying Logic: Rebalancing of Pricing Power in the Industry Chain

Upstream Perspective: Enhanced raw material scarcity and smelting costs prompted enterprises to narrow discounts and maintain firm offers.

Downstream Considerations: Slowing demand growth increased cost control pressure for battery enterprises, resulting in low acceptance of narrower discounts for secondary refined lead while seeking extended settlement cycles.

Market Expectations: Lead price volatility may intensify in 2026, weakening the hedging function of long-term contracts and constraining the flexible operations of secondary lead smelters.

The transformation of the secondary lead long-term contract market in 2026 is by no means accidental; it is an inevitable outcome of the upstream and downstream segments of the industry chain re-establishing equilibrium under new market conditions. The narrowing of the price spread reflects the objective transmission of upstream cost pressures, the adjustment in the long-term-to-spot ratio indicates a shift in market participants' risk appetite, and the divergence in enterprise contracting signals a profound realignment of the industry's competitive landscape.

Looking ahead, the secondary lead long-term contract model is expected to undergo further adjustments: first, pricing mechanisms will become more flexible, with stronger linkage to spot market prices; second, contract cycles may shorten, with quarterly and monthly long-term contracts accounting for a larger share; third, regional price differences may widen, leading to differentiated pricing based on local supply-demand conditions. Amid these changes, striking a balance between ensuring stable production operations and managing price risks will become a critical challenge for every market participant.

![The Most-Traded SHFE Lead 2604 Contract Posted a Small Bullish Candlestick, With the Tug-of-War Between Sellers and Buyers Driving Short-Term Volatility [SHFE Lead Brief Commentary]](https://imgqn.smm.cn/usercenter/lIHfM20251217171721.jpeg)

![US Dollar Index Approached 100, LME Lead Fell to a 10-Month Low [SMM Lead Morning News]](https://imgqn.smm.cn/usercenter/PKFMX20251217171721.jpg)